%20(300%20%C3%97%20300%20px)-8.avif)

-33.jpeg)

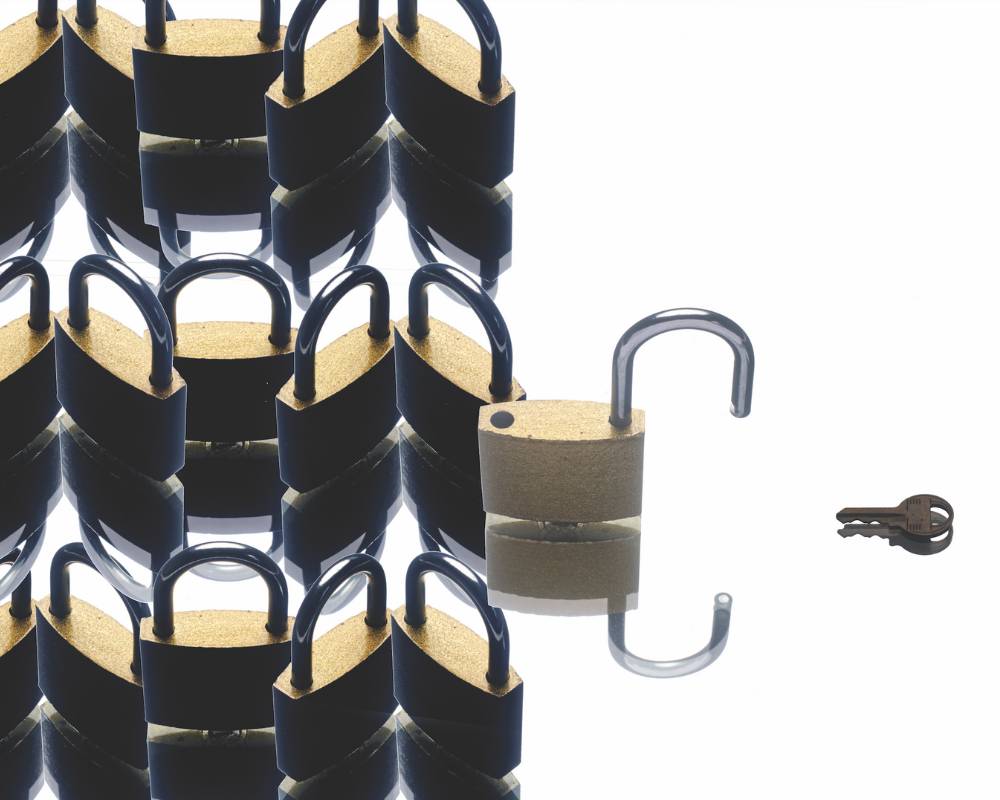

Managing uncertainty in our businesses is more critical today than ever before. Balancing opportunities and risks has always been key for our business success. In the wake of the COVID-19 pandemic, and its consequent human and systemic impacts, uncertainty remains a driving theme, and our businesses are evolving with the changing dynamics. As we progress through 2023, we are faced with more uncertainty, inflationary markets, a continued war in Ukraine, financial instability, human and resource challenges, and the impacts of climate change. Those businesses that have systems in place to manage these and other risks will not only survive but thrive.

Relevance of Insurance

In Barbados the application of insurance has been questioned in the wake of the industry response to the COVID-19 pandemic, the Soufriere ashfall from St Vincent and the impact from Hurricane Elsa in 2021. Coverage restrictions, and policy retentions, limited the policy response to claims from these recent destructive events. Insurance continues to play a fundamental role in securing your future. However, it is the final chapter in a disciplined risk management process in which your risks should be prioritized, cost effective controls implemented, and the catastrophic losses that cannot be financed otherwise, transferred to the insurance market. As a financing tool it is not without its limitations, and these must be fully understood and planned for in your approach. For your business, the security that insurance provides allows you to release funding for your investment opportunities.

Negotiating the Current Market

The insurance industry, like most operating in this difficult environment, is impacted by global uncertainty. Market volatility affects the performance of their investment portfolios established to fund losses. There is a direct correlation in increased likelihood of insurance claims with tough economic times. The costs of claims rise with the inflationary environment, supply chain costs and issues impact the logistics around the settlement of claims. Climate change is leading to increased natural disasters in terms of likelihood and costs. These among other factors have led globally to a current hard insurance market cycle. This cycle is characterized by a reduction to insurance supply as carriers withdraw cover from unprofitable lines of business, specific geographies or sectors, premium increases and more restrictive coverage terms. Reports coming from many quarters suggest increases in property and motor rates of about 10% or more as the year progresses.

What Next

Faced with this tough environment, how does one not just survive but thrive? As indicated, insurance must be considered properly as part of a disciplined risk management process otherwise you may be allocating your risk financing effort and funding to noncritical areas. Leveraging your advisors starts with a thorough analysis of your risk profile, the key risks priorities will likely have changed in the current environment and focusing on those most critical will allow you to control costs and resources. Improve your risk profile through cost-effective risk control activities. Commence your insurance renewals 4-5 months in advance and work with your advisors to review your minimum acceptable limits of liability and insurance values ensuring that these are adequate. Further build understanding of your coverage terms and limitations so that plans can be made for any gaps. Review your insurers financial position ensuring that they remain stable given the environment and can respond in your time of need. Obtain and analyze alternative options to help you manage costs, once you have good control over the risk assume higher retentions/ deductibles or self-insure. The peace of mind from your thorough risk management programme will allow you to focus on those growth and investment opportunities and ultimately thrive.

Gregory Rose

Group CEO, Malcolm Investment Holdings Ltd.

Director, Lynch Caribbean Ltd.

Latest Edition